Chart of Accounts: Setup Guide with Examples

So, when setting up your accounting system, you create the COA in this order. In the United States businessesand organizations widely use a standardized chart of accounts. Meanwhile, let’s look at the general ledger real quick because general ledger uses the accounts listed in the chart of accounts to record and organize financial transactions. The chart of accounts, at this point, serves as a structure under which the general ledger operates. The chart of accounts (COA) is a list of accounts a company uses to record its financial transactions.

Where’d you go to find equity?

Now that we have the high-level information behind us, let’s roll up our sleeves a bit and zero in on building the ideal chart of accounts for your company. As we said before, an effective COA begins with two essential building blocks – balance sheet accounts and income statement accounts. The structure of the chart of accounts makes it easier to locate specific accounts, facilitates consistent posting of journal entries, and enables efficient management of financial information over time. The COA helps businesses manage their money wisely, giving them a tool for keeping track of cash flow, creating accurate financial reports, facilitating budgeting, and cost control. So, a chart of accounts, as mentioned, organizes a company’s finances in an easy-to-understand way. It helps everyone in the company know exactly where the money is coming from and where it’s going.

Compliance and standardization

- The general rule for adding or removing accounts is to add accounts as they come in, but wait until the end of the year or quarter to remove any old accounts.

- However, the chart of accounts plays a critical role in how your revenue accounts, for instance, flow into the profit and loss statement.

- Instead, each entity has the flexibility to customize its accounts chart to fit the specific individual needs of the business.

- Use that information to allocate resources to more profitable parts of your business and cuts costs in areas that are lagging.

- To do this, she would first add the new account—“Plaster”—to the chart of accounts.

Some businesses can indicate COGS, gain and losses, etc., as separate accounts to structurize their finances even more granuarly. To understand the chart of accounts, you might want to look at the concepts of accounts and general accounting software: email settings in xero ledger. To do this, she would first add the new account—“Plaster”—to the chart of accounts. Instead of recording it in the “Lab Supplies” expenses account, Doris might decide to create a new account for the plaster.

Give Some Love to COA

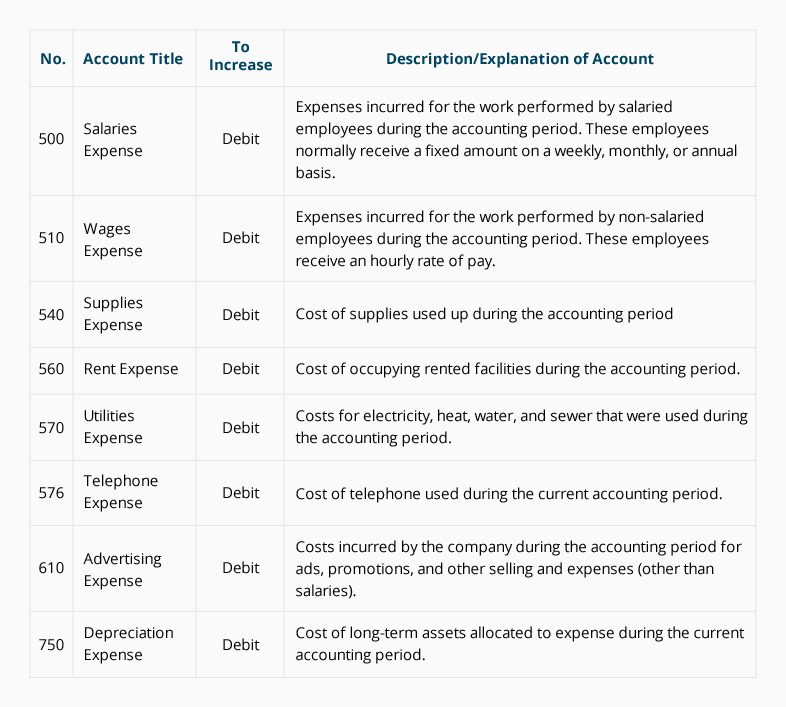

It also includes account type definitions along with examples of the types of transactions or subaccounts each may include. Many organizations structure their COAs so that expense information is separately compiled by department. Thus, the sales department, engineering department, and accounting department all have the same set of expense accounts. Examples of expense accounts include the cost of goods sold (COGS), depreciation expense, utility expense, and wages expense. There are many different ways to structure a chart of accounts, but the important thing to remember is that simplicity is key.

Example Chart of Accounts Numbering For Large and Small Companies

Granted, by the time they hit your financial reports, you’re probably grouping them in a line item anyway. However, the chart of accounts plays a critical role in how your revenue accounts, for instance, flow into the profit and loss statement. That’s what your company faces without a well-organized chart of accounts. It’s like wandering through a complex and sprawling city in search of a financial needle in a haystack. For starters, your accounting data can quickly become unreliable and outdated, which is an especially poor turn of events when timely insights are essential. In the sample chart of accounts for example, the expense accounts are sub-divided into business functions such as research and development, sales and marketing, and general and administrative expenses.

What Is General Ledger Reconciliation: Types, Best Practices and Importance

This helps ensure consistency and comparability in financial reporting. As mentioned, all accounts in the COA are typically arranged in a hierarchical order for easy navigation and reporting. It often follows a pattern where the first digit represents the major category, and subsequent digits provide more detail. Expenses are typically found on the income statement alongside revenue. Expenses are subtracted from revenue to calculate net income – the company’s profit or loss in the period in question.

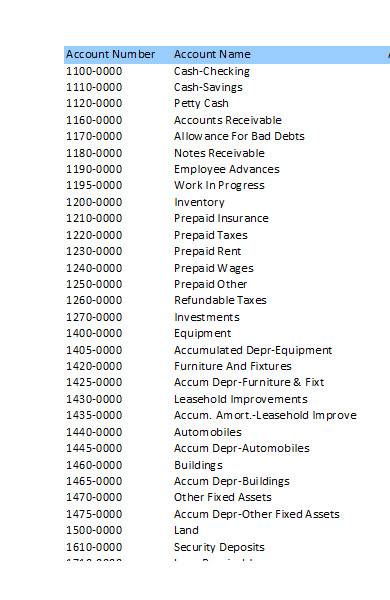

But experience has shown that the most common format organizes information by individual account and assigns each account a code and description. What’s important is to use the same format over time for the consistency of period-to-period and year-to-year comparisons. As you can see, each account is listed numerically in financial statement order with the number in the first column and the name or description in the second column. Asset accounts can be confusing because they not only track what you paid for each asset, but they also follow processes like depreciation.

Each account within the COA is typically assigned a unique identifier, usually a numerical code (see examples below), to facilitate data entry and reporting. Each type of chart of accounts serves a specific purpose, helping businesses manage their finances in different contexts—whether it’s day-to-day management, tax preparation, or compliance with legal standards. By selecting the appropriate type of COA, businesses can achieve more accurate and efficient financial management. Chart of accounts (COA) is a financial tool that acts like an index for a business’s financial transactions.

The general ledger is the central hub where all financial transactions are recorded. It contains individual account summaries, showing debit and credit entries to each account. Your chart of accounts is a living document for your business, meaning, over time, accounts will inevitably need to be added or removed. The general rule for adding or removing accounts is to add accounts as they come in, but wait until the end of the year or quarter to remove any old accounts.

It doesn’t include any other information about each account like balances, debits, and credits like a trial balance does. The chart of accounts streamlines various asset accounts by organizing them into line items so that you can track multiple components easily. Create unique account numbers and names for each account in your chart of accounts. Ensure that each account number and name is descriptive and easy to understand.